In Hawaii, summer means hurricane season. By the time a storm is approaching, it's too late to think about insurance coverage or home upgrades. With forecasts calling for an active 2026 hurricane season, now is the time to review your coverage, strengthen your home and gather essential supplies.

What Forecasters Expect for the 2026 Hawaii Hurricane Season

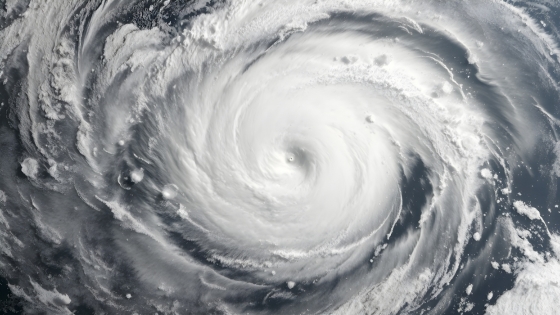

The Hawaii hurricane season runs from June to November. This year, it could be bad.

NOAA is predicting a 70% chance of above-normal hurricane activity in the central Pacific region. According to KHON 2, a strong El Niño weather pattern is expected to result in warmer conditions. As a result, Hawaii could see more than twice as many storms as usual. The last strong El Niño occurred in 2015, a record-setting hurricane season.

Understanding Hurricane Risks

A hurricane can bring strong winds, torrential rain, storm surges and sometimes even tornadoes. In addition to the physical damage caused by flooding and wind, hurricanes can also trigger power outages and cut off transportation lines, leaving people to deal with the aftermath of the storm on their own.

Hurricane Iniki struck Hawaii in 1992 – another El Niño year – and earned a place in history as the most destructive hurricane to hit Hawaii. According to the Hawaii Department of Defense, the storm brought 145 mile-per-hour winds and destroyed or damaged 70% of the homes and businesses on Kauai, as well as more than 560 homes on Oahu and 32 homes on the Big Island.

Hawaii Homeowners Need More Than Standard Homeowners Insurance

In Hawaii, a standard homeowners insurance policy will not provide the coverage you need to rebuild after a hurricane. Homeowners need three policies:

- Homeowners insurance provides coverage for many perils, including fire, theft, and vandalism. However, it excludes flood and hurricane wind damage. Claims scenario: If you evacuate your home during a hurricane, and someone breaks in and steals your valuables while you’re away, report the loss to your homeowners insurer.

- Flood insurance provides coverage for flooding, including storm surges. It can be purchased through the National Flood Insurance Program (NFIP) or through private insurance companies. Claims scenario: If a storm surge floods your home, resulting in severe damage to your house and personal belongings, report the loss to your flood insurer.

- Hurricane insurance provides coverage for wind damage associated with hurricanes. Claims scenario: If hurricane winds tear the roof off your home, allowing rain to enter your home and cause additional damage, report the loss to your hurricane insurer.

If you have a mortgage, your lender may require you to maintain homeowners insurance, flood insurance and hurricane insurance. If you don’t have a mortgage, the choice is yours – but consider whether you would have the funds needed to rebuild after a storm without insurance.

How to Prepare for Hurricane Season

With hurricane season upon us, it’s time to verify that you’re ready for a storm.

- Check your insurance. Reviewing your coverage before hurricane season can help prevent costly surprises during the claims process and ensure you have the financial resources needed to recover after a major storm. Verify that you have sufficient coverage in place, checking both the types of coverage and the limits.

- Take proactive steps to make potential claims easier. In case you need to file a claim, it’s helpful to have your insurance documents and information handy. Consider storing a digital copy of your insurance documents in a secure online storage space and a physical copy in a secure, waterproof location. A current home inventory can also simplify the claims process.

- Consider home upgrades. Certain home upgrades can increase the chance that your house will survive a storm. The Hawaii Emergency Management Agency provides several suggestions, including a hip roof design made with wind-resistant materials, such as metal, metal clips that secure the roof to the walls and the walls to the foundation, and impact-resistant windows and doors. Also inspect your home for vulnerabilities and seal any cracks or gaps that could allow wind or water intrusion.

- Gather your supplies. After a hurricane, you may not be able to buy supplies for a while, so it’s important to have sufficient food, water and medicine on hand. You should also have emergency supplies, such as a first aid kit and flashlights, as well as materials to board up windows if necessary. See Ready.gov for more information on building an emergency kit.

- Watch the forecast. You can sign up for emergency alerts. If a storm is coming, focus on safety first. If you are sheltering in your home, cover your windows if you have time, and shelter in an interior room, closet or hall away from windows.

Recovering from a hurricane can be costly, especially if coverage gaps are discovered after the storm. Reviewing your homeowners, flood and hurricane insurance now can help protect your property and financial future. An independent insurance agent can help you assess your risks and make sure you have the coverage you need before hurricane season intensifies. Find an agent.